If you searched 'NJ grow tax credit' hoping to find a cannabis-specific cultivation tax break, here is the direct answer: New Jersey does not have a standalone tax credit designed exclusively for cannabis growers. What it does have is the Grow New Jersey Assistance Tax Credit, a jobs and capital investment incentive that a licensed cannabis cultivator could potentially qualify for, but it is a business economic development credit, not a cannabis-specific grow credit. Understanding that distinction upfront will save you a lot of time.

NJ Grow Tax Credit Guide for Cannabis Cultivators

Marcus Whitley

21 Apr 2026

What the NJ Grow Tax Credit Actually Is

The Grow New Jersey Assistance Tax Credit was created by P.L. 2011, c.149 (signed January 5, 2012) and is codified at N.J.S.A. 34:1B-242 et seq. It is administered through the New Jersey Economic Development Authority (NJEDA) and is technically a corporate business tax (CBT) credit. The program was designed to encourage businesses to create or retain full-time jobs in New Jersey and to make significant capital investments in qualified incentive areas of the state.

A licensed cannabis cultivator is a business entity like any other, so if your cultivation operation meets the program's investment and employment thresholds, you could apply for and receive a Grow NJ tax credit certificate. That certificate is then used to claim the actual credit on your NJ CBT return. The program is not automatic, and it is not triggered by simply holding a cannabis grow license. It requires a separate NJEDA application, approval, and certificate issuance before any tax credit can be claimed.

One important thing to clear up: the Social Equity Excise Fee (SEEF) that cannabis cultivators pay monthly via Form SF-100 is completely separate. That is a fee, not a credit. Do not confuse the two. Similarly, there is no state income tax exemption or deduction specifically tied to holding a Class 1 Cannabis Cultivator license in New Jersey.

Eligibility Checklist for NJ Cultivators

Before you spend time on an NJEDA application, run through these eligibility conditions. This is a practical checklist, not a replacement for reading the actual statute or talking to a tax professional.

- Business entity status: You must be a business entity subject to New Jersey Corporate Business Tax, not an individual filer. Sole proprietors claiming on personal income tax returns use a different pathway (Form 320-IPT for insurance premium tax filers).

- License status: While holding an active NJ cannabis cultivator license does not by itself qualify you, it confirms you are operating a legitimate business in the state, which is a baseline requirement.

- Qualified incentive area: Your cultivation facility must be located in an NJEDA-designated qualified incentive area. Not every location in NJ qualifies automatically, so verify your address against NJEDA's current area designations.

- Capital investment threshold: The program requires a minimum capital investment, with the Division of Taxation's guidance referencing a $20,000,000 minimum as a benchmark. Smaller operations are unlikely to meet this threshold.

- Job creation or retention: You must be creating or retaining full-time New Jersey-based jobs. The credit is calculated on a per-job basis, and the number of qualifying jobs drives the credit amount.

- NJEDA approval and certificate: You must have applied to the NJEDA, been approved, and received an official Grow NJ tax credit certificate before any credit can be claimed on your tax return.

- Ongoing employment maintenance: Once approved, you must maintain at least 80% of the employment level that was the basis for the credit. Dropping below that threshold results in forfeiture of that year's credit amount.

If your cultivation operation is a micro grow or a smaller licensed business, the capital investment and job thresholds make qualifying for Grow NJ very difficult. For a micro grow, you should also plan for how the license cost and capital requirements can affect whether you realistically meet the Grow NJ thresholds micro grow license cost. For context on what a micro grow license looks like in NJ and its associated costs, the licensing structure itself gives useful framing around the scale of qualifying operations.

How to Actually Claim the Credit

Step 1: Apply through NJEDA first

The process starts entirely outside of the tax system. You must submit an application to the NJEDA, demonstrate that your facility meets the qualified incentive area requirement, commit to the required capital investment, and show a qualifying job creation or retention plan. NJEDA will evaluate your application, and if approved, they will issue an award agreement and, once investment and employment conditions are met and certified, a tax credit certificate.

Step 2: Receive and verify your tax credit certificate

The eligibility period begins with the tax period in which NJEDA accepts certification that both your capital investment and employment requirements have been satisfied. At that point, NJEDA issues the Grow NJ tax credit certificate that specifies your credit amount. That certificate is your core document. Without it, you cannot claim the credit.

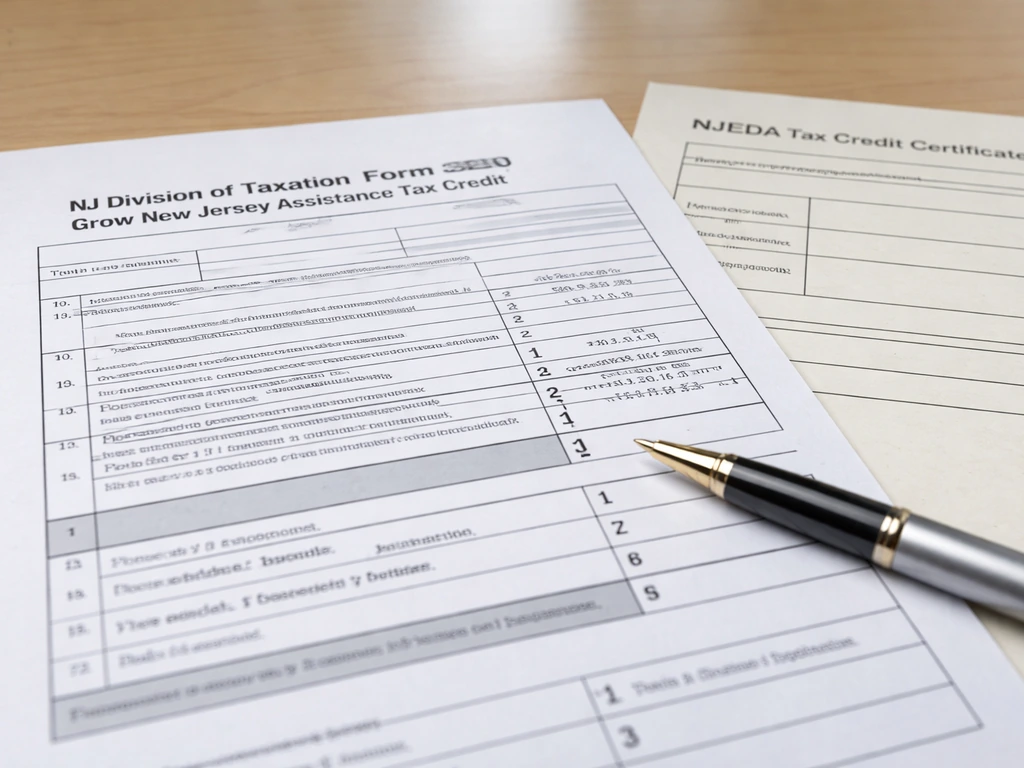

Step 3: Complete Form 320 with your CBT return

To claim the credit on your corporate business tax return, you must complete NJ Division of Taxation Form 320 (Grow New Jersey Assistance Tax Credit). To get your records in order, make sure you have your grow therapy tax ID number available when working through the Grow NJ credit paperwork. This form must be included with your CBT-100, CBT-100S, or CBT-100U return when you file. Failing to include it means the credit claim is not validated.

Step 4: Mail the required documentation separately

In addition to filing electronically, you must also mail a copy of the tax credit certificate along with a completed copy of Form 320 to the NJ Division of Taxation at the CBT Refunds/Tax Credits unit. This mailing step is separate from your return filing and is explicitly required by the Form 320 instructions. Skipping this step can delay or deny your credit claim even if your return was filed correctly.

For pass-through entities and insurance premium taxpayers

If you are a pass-through entity claiming on the insurance premium tax side, the applicable form is Form 320-IPT. The same logic applies: attach Form 320-IPT to your return, and separately mail a copy of the tax credit certificate (or tax credit transfer certificate, if you received a transferred credit) along with the completed form to the NJ Division of Taxation's Special Audit, Insurance unit.

Key documentation to gather

- Original NJEDA Grow NJ tax credit certificate (or transfer certificate if applicable)

- Completed Form 320 or Form 320-IPT

- Your NJ cannabis cultivator license documentation (Class 1 license from the Cannabis Regulatory Commission)

- Business formation and tax ID documentation

- Records showing qualifying full-time job counts for the credit year

- Capital investment documentation (receipts, asset records, etc.) confirming you met the investment threshold

- Your completed CBT return (CBT-100, CBT-100S, or CBT-100U)

Credit Amounts, Caps, and Common Misconceptions

The credit amount is determined by what is stated on your NJEDA-issued tax credit certificate, not by a calculation you make yourself. It is tied to the number of qualifying jobs and related parameters set during the NJEDA award process. If the qualified business facility’s full-time New Jersey workforce falls below the corresponding 80% threshold, the business forfeits the tax credit amount for that tax period and subsequent tax periods until the workforce/jobs are restored to the minimum level and approved by the NJEDA Board the 80% job retention threshold. For any given business, the credit available in a tax period is capped at the lesser of one-tenth of the qualifying capital investment or $4,000,000. So even if your investment is enormous, the annual per-period credit tops out at $4,000,000.

If the credit exceeds your tax liability in a given year, Form 320 includes a Part III carryforward section for CBT-100 and CBT-100S filers, meaning unused credit amounts can be carried forward to future tax periods rather than being lost. For context on what people find confusing about the NJ CBT-100S-related tax calculation and how the CBT-100S return interacts with NJEDA-based credit reporting, a Reddit discussion thread lays out common confusion points and practical takeaways blank" rel="noopener noreferrer">common confusion points about the NJ CBT-100S-related tax calculation and how the form interacts with entity-level taxation. The Form 320 instructions also include check boxes to indicate whether you received a tax credit certificate or a credit transfer certificate issued by NJEDA and provide fields to compute the credit using CBT tax liability inputs blank" rel="noopener noreferrer">Form 320 includes a Part III carryforward section.

When you are claiming multiple credits in the same CBT return period, the Form 320 instructions require you to list all other credits already applied against your tax liability before calculating what Grow NJ credit remains usable. This interaction calculation matters because you cannot use more combined credit than your total tax liability allows.

Misconceptions that waste time

- Misconception: The credit is automatic once you have a grow license. Reality: You need a separate NJEDA application, award, and certificate. The cannabis license alone does nothing here.

- Misconception: Individual cannabis growers or home cultivators can claim this. Reality: This is a corporate business tax credit. Individual filers do not qualify via the standard CBT pathway.

- Misconception: The SEEF or other cannabis-specific fees offset against a 'grow tax credit.' Reality: The SEEF is a separate fee obligation with no connection to the Grow NJ credit program.

- Misconception: The credit amount is whatever you calculate it to be. Reality: The amount is fixed by your NJEDA-issued certificate. Self-calculated claims not backed by a certificate will not hold up.

- Misconception: Transferring unused credits is not an option. Reality: Unused credits can, in some cases, be transferred via a credit transfer certificate, which then changes the form and mailing procedures.

Compliance Considerations for Cannabis Cultivators

Pursuing the Grow NJ credit while maintaining your cannabis cultivation license requires keeping both tracks clean and separate. Your NJ Cannabis Regulatory Commission (CRC) license is governed by cannabis-specific operating rules, and your tax credit program is governed by NJEDA award conditions and Division of Taxation requirements. A problem in one does not automatically cause a problem in the other, but there are overlapping concerns to manage.

- Maintain your license in good standing: A suspended or revoked cannabis cultivator license could affect your standing as a legitimately operating business, which NJEDA may consider when reviewing ongoing certification of your award.

- Keep employment records accurate: The 80% employment retention threshold is a real forfeiture trigger. If staffing levels drop, you could lose credit for that period even if all other conditions are met.

- Stay current on SEEF reporting: Monthly SF-100 filings for cultivators are a separate compliance obligation. Falling behind on those creates tax exposure that could complicate your overall NJ tax standing, which in turn affects your CBT filing.

- Document capital investments carefully: NJEDA may audit investment claims during the eligibility period. Keep all asset purchase records, construction costs, and related documentation organized and accessible.

- Track your credit certificate expiration: Grow NJ credit certificates cover a defined eligibility period. Once that period ends, unused carryforward credit may be the only remaining option. Check your certificate's effective dates.

- Avoid mixing incentive programs: If you are receiving other NJEDA grants or incentives, there may be interaction rules that limit or modify your Grow NJ credit. The Division of Taxation's CBT credits framework notes restrictions when businesses participate in certain other incentive programs.

It is also worth noting that a cannabis cultivator license (Class 1 in NJ) does not grant any special tax treatment by itself. If you are looking for a “grow tax free” path, the key is understanding whether you qualify for the Grow NJ tax credit and how it applies to your CBT return. The NJ Division of Taxation's cannabis-focused publication ANJ-30 makes clear that financial incentives are separate from operating permissions. Having a license does not mean you automatically receive any credit, and applying for a credit has no bearing on your licensing status with the CRC.

Where to Verify the Latest Rules

Tax credit programs change, and the details here reflect the program as it stands in early 2026. Before taking any action, verify the current program status, amounts, and deadlines using these official sources directly.

| Resource | What to Use It For | Where to Find It |

|---|---|---|

| NJ Division of Taxation – Form 320 Instructions | Confirm current claim mechanics, mailing requirements, and carryforward rules for CBT filers | NJ Division of Taxation website, Corporate Business Tax forms section |

| NJ Division of Taxation – Form 320-IPT Instructions | Confirm procedures for pass-through/insurance premium tax filers | NJ Division of Taxation website, Corporate Business Tax forms section |

| NJEDA Grow NJ Program Page | Verify program eligibility criteria, qualified incentive areas, and application status | NJEDA.com, Grow New Jersey Assistance Program section |

| NJ Division of Taxation – CBT Credits List | Understand interaction rules, forfeiture conditions, and transfer certificate options | NJ Division of Taxation website, Corporation Business Tax Credits and Incentives page |

| NJ Division of Taxation – ANJ-30 (Cannabis Publication) | Cross-reference cannabis-specific tax obligations separate from Grow NJ credit | NJ Division of Taxation website, cannabis tax publications |

| NJ Division of Taxation – Cannabis License Information Page | Confirm your license class and standing with state tax authorities | NJ Division of Taxation website, Recreational Cannabis section |

| NJEDA Public Information / Award Reports | Validate that your NJEDA award is on record and the certificate amount is confirmed | NJEDA.com, Public Information section |

One practical step worth taking: before filing, call or write the NJ Division of Taxation's CBT Refunds/Tax Credits unit directly to confirm the current mailing address and any procedural updates. Form instructions can lag behind process changes, and confirming the submission requirements directly prevents avoidable rejections.

Nothing in this article is legal or tax advice. The rules around the Grow NJ credit are detailed enough that if you believe your cultivation business qualifies, working with a New Jersey-licensed CPA or tax attorney who knows the NJEDA incentive programs is strongly worth the cost. The credit amounts can be substantial, but the compliance requirements are equally serious.

FAQ

What’s the biggest reason an NJ grow tax credit (Grow NJ) claim gets rejected even if I have a tax credit certificate?

Most denials happen when the certificate details and the return form inputs do not match exactly, or when the required separate mailing is skipped. Keep a single folder with your NJEDA tax credit certificate, the completed Form 320, your CBT return version (CBT-100/100S/100U), and the proof of mailing to the CBT Refunds/Tax Credits unit, then reconcile the credit amount you report to what the certificate states before you file.

If I’m a cannabis cultivator but operate through an LLC, how does that affect the nj grow tax credit claim process?

The key factor is the entity’s NJ tax classification, not just the fact that you hold a cultivation license. Your eligibility for filing Form 320 on the correct return side depends on whether you file as a corporation for NJ CBT purposes, a different structure, or you are a pass-through entity using the insurance premium tax approach. Confirm which tax return you are actually filing (and which Form 320 version applies) before you start collecting documents.

Can I claim the Grow NJ credit before NJEDA has certified that my capital investment and job requirements are met?

No. The article’s sequence matters, NJEDA issues the tax credit certificate after it accepts certification that both investment and employment conditions have been satisfied. Until you have that NJEDA-issued certificate for the relevant tax period, you generally should not treat the credit as claimable on your CBT return.

Does paying the Social Equity Excise Fee (SEEF) have any impact on my nj grow tax credit?

It should not. SEEF is a monthly fee tied to cannabis operations, it is not the Grow NJ incentive credit. Treat SEEF records as separate compliance documentation, and do not expect SEEF payments to increase, qualify, or substitute for the NJEDA-driven certificate needed to claim the corporate tax credit.

What if I have multiple Grow NJ awards or another credit program, how do I avoid using too much credit on my return?

You must account for other credits already applied against your tax liability when computing how much Grow NJ remains usable. Practically, list all credits taken in that CBT period in the order required by the Form 320 instructions, then check your total credit versus total tax liability so you do not exceed what the return math permits.

If my Grow NJ credit is more than my tax liability, how does carryforward work for a cannabis cultivator?

For CBT-100 and CBT-100S filers, Form 320 includes a carryforward section (Part III) for unused credit amounts, so the excess is not necessarily lost. Your next step is to review the Form 320 Part III entries for the correct carryforward period and ensure your future returns continue to reference and support the carryforward values consistent with your NJEDA certificate.

I received a transferred credit. What changes for the nj grow tax credit filing and mailing steps?

You typically need the tax credit transfer certificate, not just the original certificate, and you must still follow the separate mailing requirement with the correct certificate and completed Form 320. Confirm whether your paperwork reflects the transfer recipient’s information because mismatches can create a validation problem even when the certificate is present.

What’s the best way to confirm I have the correct grow therapy tax ID number needed for Form 320?

Use the same ID you will report consistently across your credit documentation, and verify it against your cultivation-related tax paperwork before you submit. Because Form 320 validation can be strict, double-check the ID format and number you plan to enter, then keep that value tied to your NJEDA application records so it does not differ between documents.

If I’m a micro grow, should I still apply for the nj grow tax credit, or will the thresholds automatically make it impossible?

Micro grow scale can make the investment and job thresholds difficult to meet, but it is not always automatically impossible, it depends on the specific numbers in your NJEDA application for capital investment and the qualifying job plan. Your practical next step is to model whether you can realistically satisfy the threshold conditions and then compare that to the credit cap mechanics on your expected certificate amount.

Does applying for the Grow NJ credit affect my cannabis cultivator license status with the NJ CRC?

Generally, no. License permissions and regulatory compliance are handled by the CRC, while the Grow NJ program is administered by NJEDA with tax filing rules enforced by the Division of Taxation. However, keep both records clean because a compliance issue in either system can affect your ability to meet award certification requirements over time.

Next Article

NJ Grow License: From Zero to Submitted in New Jersey

Step-by-step NJ grow license guide: eligibility, license types, legal requirements, costs, application steps, and next a